What I Wish I Knew in My Twenties

When I was in school, no one ever taught me about financial literacy. I didn’t know what tools were available, why I should have an emergency fund, or even how to properly pay off a credit card. It wasn’t until I got older (and a few money mistakes later) that I realized how important financial wellness really is.

The truth is, many jobs don’t offer pensions anymore, so it’s up to us to take control of our savings and plan for the future. That might sound intimidating, but it doesn’t have to be! My goal is to share simple and realistic tips to help you start taking those first steps toward financial confidence. Together, we can make this journey a little less daunting and maybe even fun!

Let’s dive in!

A Quick Note

This isn’t a full financial literacy course. It’s a collection of tips and real-life examples I wish I had when I was younger. If you want to dive deeper, check out the Government of Canada’s Financial Toolkit.

It’s free and super helpful: Financial Toolkit.

https://www.Canada.ca/en/financial-consumer-agency/services/financial-toolkit.html

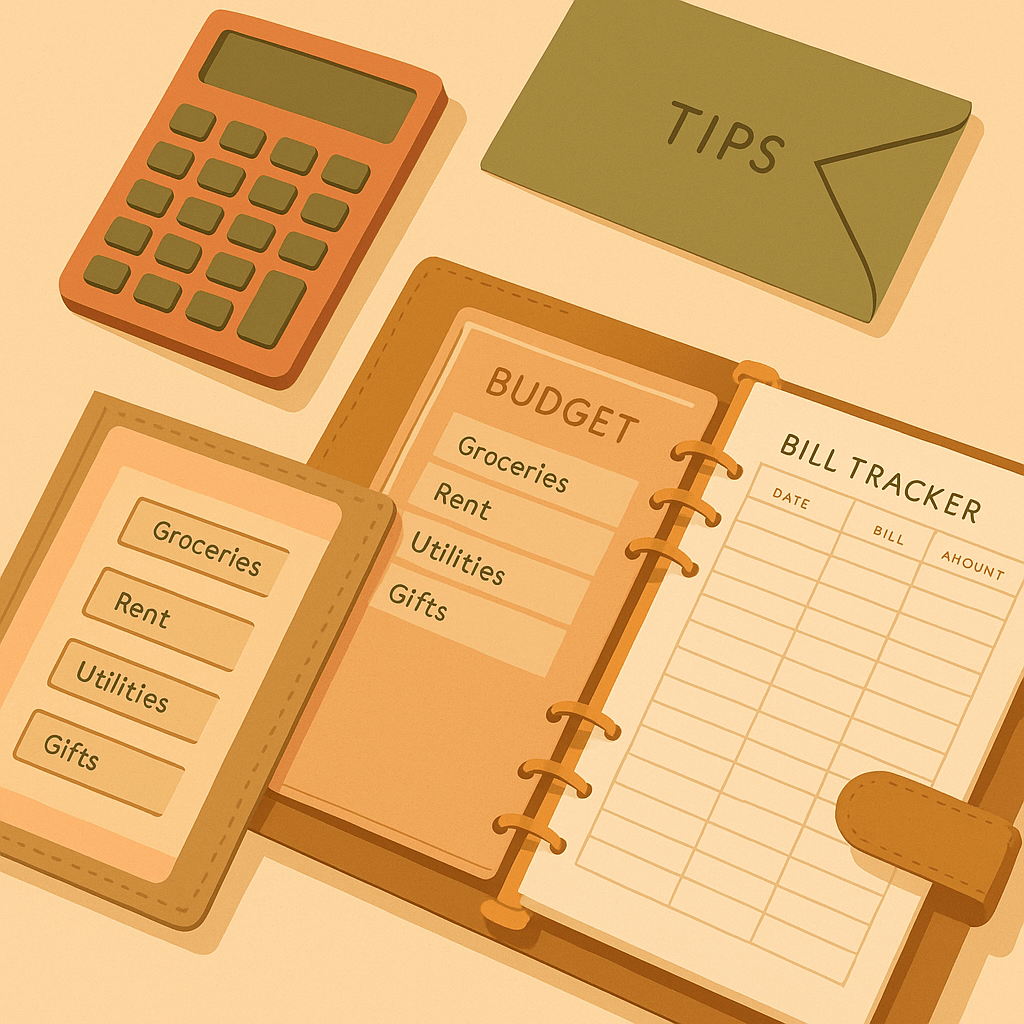

Step 1: Learn to Budget

Budgeting is one of the best ways to take control of your money. It’s not about restricting yourself — it’s about understanding where your money is going and making decisions that work for you.

Here’s an example of how to build a basic monthly budget:

Income:

Let’s say you take home $2,500 per month after taxes

Fixed expenses (stay the same):

$1,000 rent

$400 car payment and insurance

$150 utilities

Total: $1,550

Variable expenses (change month to month):

$400 groceries

$250 entertainment

$100 gas

Total: $750

Remaining:

$2,500 income

– $1,550 fixed expenses

= $950 left over

– $750 variable expenses

= $200 left

You now know you have $200 to play with, or put toward savings or debt.

If you’re finding there’s nothing left, or you’re going into debt each month, that’s a sign to revisit your variable spending. Could you adjust your entertainment budget or cut back on dining out?

A lot of experts recommend saving at least 20 percent of your income but I know that number can feel big when you’re just starting (it sure did for me). Don’t let that stop you. Start small and build up. Five dollars in the right direction is still five dollars better than before.

Step 2: Understand Compound Interest

Compound interest is one of those things that sounds boring — but once you understand it, it’ll change how you see money. It’s the reason starting early matters so much.

Here’s the difference between simple interest and compound interest:

Simple interest means you only earn interest on the original amount you put in.

Compound interest means you earn interest on your original amount and the interest you’ve already earned.

Let’s say you invest $1,000 at 5 percent annual interest.

With simple interest:

You earn $50 a year, every year.

After 5 years: $250 total interest

With compound interest:

Year 1: $50

Year 2: $52.50

Year 3: $55.13

Year 4: $57.88

Year 5: $60.88

After 5 years: $276.38 total interest

It doesn’t seem like a huge difference but over longer periods of time, it adds up. After 10 years, you’d have $628. After 50 years? Over $10,000, from just a one-time $1,000 investment.

The earlier you start, the more time your money has to grow.

The Dark Side of Compounding: Credit Cards

Unfortunately, compound interest also works against you when you’re in debt.

Credit cards can be useful when used wisely but they’re dangerous if you carry a balance. Most cards give you a 21-day grace period to pay off your balance in full without paying interest. If you miss that, interest starts to build and it compounds monthly.

Interest rates in Canada are usually between 19 and 23 percent. If you have a $40,000 balance at 20 percent interest, you’ll owe about $8,000 in interest in one year alone. And that interest starts stacking on itself, making it harder and harder to get ahead.

Key takeaway: Use credit cards as a tool, not a fallback. Try to pay them off in full every month so interest never kicks in. If you do carry a balance, focus on paying it down as soon as you can.

RRSP vs TFSA: What’s the Difference?

In Canada, two of the best savings tools are the RRSP and the TFSA. They both help you grow your money and reduce taxes, but they’re used differently.

RRSP (Registered Retirement Savings Plan):

This is for future you. When you put money into an RRSP, it lowers your taxable income today. But when you take that money out in retirement, you’ll pay tax on it then.

Example:

You earn $30,000 and contribute $3,000 to your RRSP. Your income for tax purposes is now $27,000, so you owe less tax today. That $3,000 grows over time, and you’ll pay tax on it when you withdraw it in the future.

TFSA (Tax-Free Savings Account):

This is a flexible savings account. You put in after-tax dollars, and whatever it earns, interest, dividends, or growth, is completely tax-free, even when you withdraw it.

Example:

You save $3,000 in a TFSA, and it grows to $4,000. When you take it out, you keep the full $4,000, no tax owed.

So which is better?

If you’re making a lower income (like $30,000 or less), a TFSA is often more beneficial because you’re not saving a ton on taxes with an RRSP anyway. You can still contribute a bit to your RRSP to reduce taxes and use your refund to boost your TFSA savings.

Think of an RRSP as saving for “Future You” and a TFSA as saving for “Anytime You.” They both have their place, and using them together can help you build real financial security.

Final Thoughts: Financial Wellness Is a Practice

Money can be stressful. But understanding how to work with what you have makes it a whole lot less scary.

Financial wellness isn’t about being perfect or rich. It’s about being intentional. It’s learning to plan, spend, save, and adjust with care. It’s setting goals, tracking your progress, and forgiving yourself when you mess up.

Treat this like you would any other kind of wellness — a work in progress. Some weeks you’ll be on top of it. Some weeks, not so much. That’s okay.

Start small. Stick with it. And trust that every little effort you make adds up.

If you want more info or tools to dive deeper, the Government of Canada’s Financial Toolkit is a great place to start:

https://www.canada.ca/en/financial-consumer-agency/services/financial-toolkit.html

Leave a comment